| 12-04-2019, 04:05 PM | #89 | |

|

OPN DIFF

497

Rep 1,918

Posts

Drives: 10' E90 M3 6MT LB

Join Date: Oct 2012

Location: Pacific Ocean

|

Quote:

__________________

'10 LB E90 slicktop/speed cloth/6MT ex. '06 330i 6MT & '10 n54 6MT Msport Autocross vids https://www.youtube.com/user/tigermack https://www.instagram.com/tigermack |

|

|

Appreciate

0

|

| 12-05-2019, 12:18 PM | #90 | |

|

Colonel

8203

Rep 2,250

Posts |

Quote:

__________________

Everybody has a gameplan....until they get punched in the mouth.

|

|

|

Appreciate

0

|

| 12-05-2019, 02:27 PM | #91 | |

|

Captain

1724

Rep 618

Posts |

Quote:

|

|

| 12-05-2019, 02:36 PM | #92 | |

|

First Lieutenant

276

Rep 308

Posts

Drives: BMW M235i

Join Date: Jun 2019

Location: Seattle, WA

|

Quote:

Last edited by grocerylist; 12-05-2019 at 02:47 PM.. |

|

| 12-05-2019, 03:05 PM | #93 | ||

|

Major General

3091

Rep 6,089

Posts |

Quote:

|

||

| 12-05-2019, 04:50 PM | #94 | |

|

Captain

1724

Rep 618

Posts |

Quote:

|

|

|

Appreciate

1

Rmtt8203.00 |

| 12-05-2019, 05:44 PM | #95 | |

|

dances with roads

5120

Rep 4,136

Posts |

Quote:

|

|

|

Appreciate

0

|

| 12-05-2019, 05:52 PM | #96 | ||

|

Major General

3091

Rep 6,089

Posts |

Quote:

|

||

|

Appreciate

0

|

| 12-06-2019, 04:18 AM | #97 |

|

2JZ-GTE

3174

Rep 4,149

Posts |

Boeing

|

|

Appreciate

0

|

| 12-06-2019, 07:56 AM | #98 | |

|

Captain

1724

Rep 618

Posts |

Quote:

|

|

|

Appreciate

0

|

| 12-06-2019, 09:57 AM | #99 | ||

|

Major General

3091

Rep 6,089

Posts |

Quote:

|

||

|

Appreciate

0

|

| 12-06-2019, 11:17 AM | #100 | ||

|

Major

1650

Rep 1,011

Posts |

Quote:

|

||

|

Appreciate

0

|

| 12-06-2019, 12:33 PM | #101 | |

|

Major General

6068

Rep 5,609

Posts |

Quote:

- Then take other money and open a Roth IRA. Again, buy mostly low expense ratio/fee S&P 500 index funds. - Then once those accounts are cranking and have 6 figures in them, then open a brokerage account and buy more low expense ratio/fee S&P 500 index funds, quality stocks and funds, and play around. - Pay off your house. Do all of this while living within your means and don't be a slave to debt or buy into the YOLO idea because the reality is you're likely living into your 70s or later.

__________________

The forest was shrinking, but the Trees kept voting for the Axe, for the Axe was clever and convinced the Trees that because his handle was made of wood, he was one of them.

|

|

|

Appreciate

2

damageprone584.50 Rmtt8203.00 |

| 02-27-2020, 10:25 PM | #102 | |

|

Second Lieutenant

82

Rep 232

Posts |

Quote:

|

|

|

Appreciate

0

|

| 02-28-2020, 09:01 AM | #103 |

|

M3

1437

Rep 725

Posts |

With the exception of the 401K I have through my employer and my wife's Vanguard account, I liquidated my Schwab brokerage and put all of the money into a CD at 2.55% for 12 months back in October. Impeachment, the coming election cycle and an unsubstantiated belief that the market was "due" for a correction drove my decision making. I figured the volatility could or would limit the potential upside in the stock market.

Even without factoring in the coronavirus drop, in hindsight, now that I see the trajectory the election cycle is taking in the Democratic Party, I'm happy I got out. Come October, I think I will be in a better position on where to invest vs. where I was last October, that's the hope at least. For now, I'm happy to keep up with inflation. |

|

Appreciate

0

|

| 02-28-2020, 11:09 AM | #104 | |

|

Lieutenant

630

Rep 451

Posts |

Quote:

__________________

2025 M340i xDrive /// Dravit Grey - Tacora Red

|

|

|

Appreciate

1

3GFX718.00 |

| 02-28-2020, 11:34 AM | #105 | |

|

Banned

860

Rep 407

Posts

Drives: Miss Daisy

Join Date: Jul 2019

Location: PA

|

Quote:

|

|

|

Appreciate

0

|

| 02-28-2020, 11:58 AM | #106 |

|

Captain

1724

Rep 618

Posts |

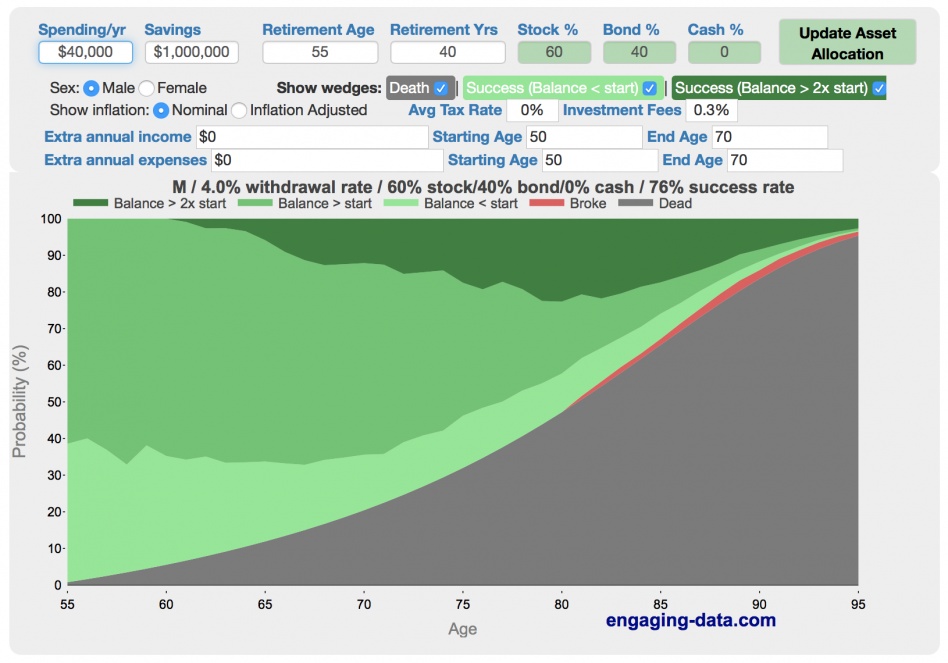

This is my favorite chart. It helps me focus on living today vs. planning for tomorrow.

Here's link if you want to play with it: https://engaging-data.com/will-money...5x=1&flexpct=0

__________________

stultorum criminis reus erit

|

|

Appreciate

5

|

| 02-28-2020, 09:53 PM | #108 | |

|

Colonel

8241

Rep 2,519

Posts

Drives: 9Y0 Cayenne S

Join Date: Mar 2019

Location: Einbahnstraße

|

Quote:

|

|

|

Appreciate

0

|

| 03-02-2020, 02:05 PM | #109 | |

|

Lieutenant Colonel

13077

Rep 1,965

Posts |

currently I would invest in surgical masks, later - toilet paper.....then I would put it deep inside my hot ass girlfriend. Next.

__________________

Quote:

|

|

|

Appreciate

0

|

| 03-02-2020, 10:36 PM | #110 | |

|

Banned

3227

Rep 2,385

Posts |

Quote:

|

|

|

Appreciate

2

King Rudi13077.00 Jordan's World429.00 |

Post Reply |

| Bookmarks |

|

|